The US economy has had several false starts since 2009, and it’s likely that several tangled factors were responsible for their not lasting longer. It’s reasonable to think that one of these factors was that the initial reflationary effects of these unconventional measures faded, because of doubts about the Fed’s commitment to maintaining accomodative policy during a period of catch-up growth. If such growth threatened to generate above-target inflation, then monetary conditions could be expected to tighten.

The rational-nerdy thing to do was to soften the macho commitment to inflation and commit to a temporary period of inflation-tolerance, thereby balancing the two sides of the mandate — but to do so while retaining credibility on both. But as Harless notes, ceding a little ground on one side could be interpreted as ceding all ground. Being a “macho badass” central banker means credibly committing to never cede ground.

…

All of which has been a long windup to saying that the appeal of the Evans Rule, and if we ever get it, some variation of NGDP level targeting, is this: they institutionalise the macho badassery, which in a dual-mandate framework can only be applied to one of the two mandates.Woj’s Thoughts - This post is reminiscent of a thread from last year involving Steve Roth and Ryan Avent on The Asymmetric Nature of Monetary Policy. In that post I made the following claim:

Whereas Roth suggests that asymmetric credibility stems from the Fed’s actions, I believe it is actually an inherent condition in our current monetary system. The Fed sets the base price for money and credit, but with private banks free to create credit, it holds relatively little control over the total amount outstanding at any time. As growth in the US has exceeded inflation for much of the past three decades, the conditions were ripe for borrowing and credit outstanding now greatly surpasses the sum of base money.

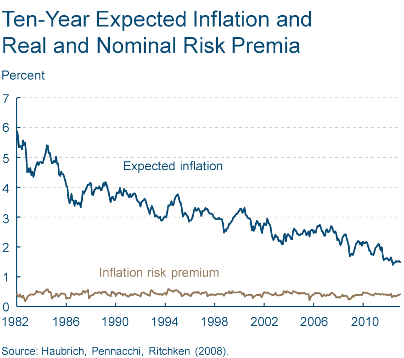

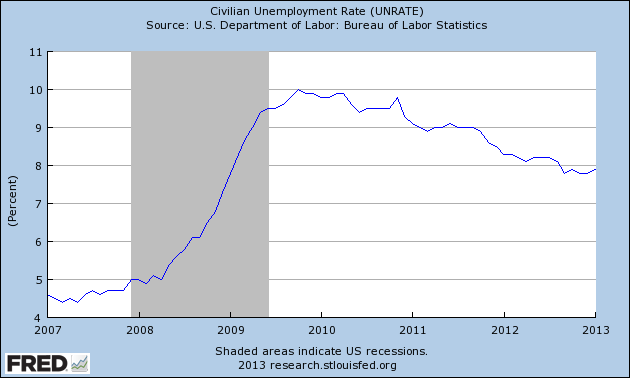

Even if the Fed promised indefinite QE, it’s hard to see the mechanism, aside from adjusting inflation expectations (wealth effects are minimal), by which this would spur real growth. Given the Fed’s skewed abilities and determination to maintain its credibility, it seems more obvious why inflation targeting remains prominent. Further, this may help explain why the Fed downplays its employment mandate (which should be removed anyways). Facing the endgame, the Fed knows it can reduce inflation (and growth) but remains unsure how successful it could be at achieving other targets.Sucumbing to pressure, the Fed has finally decided to cede ground on its commitment to inflation. Unfortunately for the Fed, both inflation expectations and unemployment are not cooperating:

At this point I doubt whether even altering inflation expectations would provide any boost to actual inflation or employment. If fiscal policy continues to contract the budget deficit, these numbers will continue moving in the wrong direction. The Fed has taken a big risk with its established credibility. I fear the results will be very disappointing.

Well, as Abraham Lincoln once said" You can fool some of the people some of the time..... How anyone paying attention to what's going on could expect inflation with unemployment at 8% is just "irrational exuberance." I think what we're seeing is that monetary policy is not efficient at fiscal policy. Monetary policy can offset excessive fiscal policy, for sure, but right now it looks as though the powers that be are intent on making fiscal policy matters more austere. Instead of trying to fix the problem with the economy there is one party that is more focused on affixing blame, at the expense of the unemployed and fixed income citizens.

ReplyDeleteNot sure if I understand you correctly, but I wouldn't go so far as saying inflation can't persist with high unemployment. Even ignoring earlier periods of actual stagflation, developed countries around the world have had persistently low, but positive inflation over the past 3-4 despite high unemployment rates (that includes Spain and Greece). IMO the chances of high rates of inflation given current levels of unemployment is pretty low, but the chances of actual deflation appear substantially lower.

DeleteShould have been a bit clearer. What I'm saying is that in our economy, the rate of unemployment has been at 8% or more since the beginning of the first Obama term. Massive amounts of liquidity have been added to the system via mostly monetary and some fiscal side efforts. Interest rates have barely moved in an upward direction, and have not shown any signs of inflation. It would seem that the concern was more about deflation than inflation by policy makers at the Fed. Granted, key consumer prices have been rising, but the question is this because of external price pressure or from excessive demand from within the domestic economy? I suspect it is from the former. The recent spike in gas prices could be the result of refiners and big oil trying to recapture some of the lost revenue as a result of the recent hurricane Sandy. Speculation on my part, but I can't see what else is driving price in this market. You?

ReplyDeleteI agree with you on inflation being driven by pricing pressure but would lean towards a more internal factor as the primary cause...debt. Most economists don't consider the interest payments on debt as part of production costs but I think that's incorrect, in accordance with many Post-Keynesians (certainly Marc Lavoie and Wynne Godley). Over the past couple decades and even throughout the crisis, nonfinancial corporation have relying increasingly on debt to fund current production. Regardless of whether these companies price at cost or use cost-plus pricing, the rising interest burden should push up prices over time. (Art Shipman at The New Arthurian Economics frequently discusses this topic.)

DeleteWoj, That's an interesting (no pun intended), observation. I'm a big fan of the Arthurian, and he is always talking about the excessive amount of private debt. I must have missed the nexus about the interest being the primary cause of rising prices. I'm sure this could be a factor. Is it the primary factor? What about the notion that prices are rising to offset the anemic consumption? Or, my observation with regard to the recent spike in gas pricing? If the mechanism is interest rates, as you say, it would seem like a good time to refinance at lower rates. But, then again, banks are unwilling to lend at rates that are in line with the cost of their own borrowing rates. Let's call it the "paradox of interest rates."

ReplyDeleterexbet

ReplyDeletepusulabet

sex hattı

rulet siteleri

hipodrombet

GYMU8F

kuşadası

ReplyDeletemilas

çeşme

bağcılar

çorlu

Q7VİK