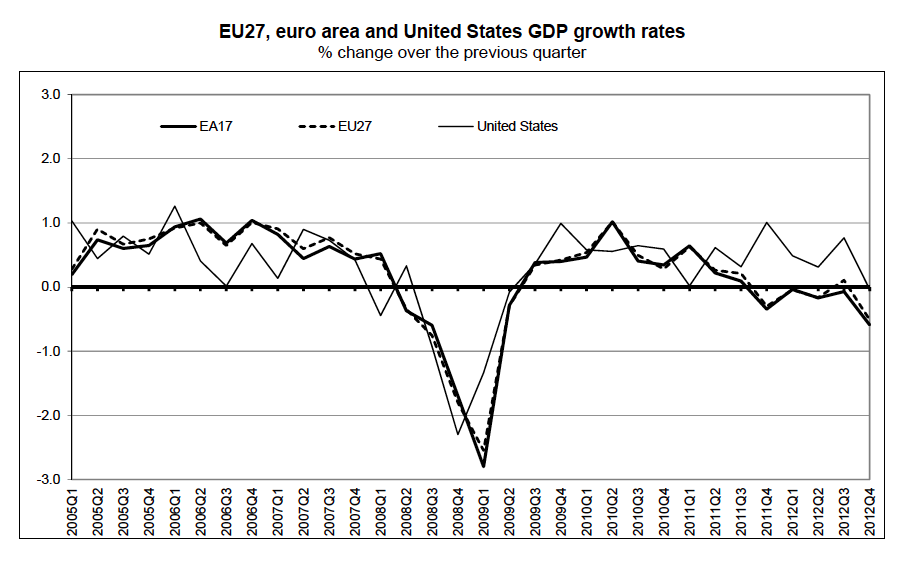

With data now confirming Europe’s awful fourth quarter on the GDP and unemployment front, it may be time to reconsider whether recent optimism is truly warranted...

Europe's A Fragile Bubble', Citi's Buiter Warns Of Unrealistic Complacency courtesy of Zero Hedge

We recognise that, in a decentralised market economy where expectations of the future, moods, hopes and fears drive private (and sometimes also government) behaviour directly and through their effect on the prices of real and financial assets, today’s subjective expectations and other psychological characteristics in part determine what tomorrow’s fundamentals will be.

Irreversible or costly-to-reverse decisions like capital expenditure, human capital formation, resource extraction etc, are driven by subjective expectations and moods, making the distinction between a fundamentally warranted asset boom and a bubble slightly fuzzy at the edges.

But this indeterminacy, bootstrapping, self-validating characteristic of complex dynamic economic systems inhabited by partially forward-looking households, firms and policy makers – called reflexivity by George Soros – can be taken too far.

Mere optimism and confidence will not permit the authors of this note to bootstrap themselves into winning the men’s doubles at Wimbledon 2013. The fact that financial markets have radically reduced their implied estimates of the likelihood of sovereign default in the periphery of the EA (other than in Greece) and of senior unsecured bank debt restructuring throughout the EA, core as well as periphery, should not stop us from continuing to analyse carefully the fundamental drivers of both sovereign credit risk and senior unsecured bank debt credit risk. When we do this, the conclusion that the markets materially underestimate these risks is, in our view, unavoidable.Woj’s Thoughts - Actions by central bankers and politicians in the Euro Area, U.S., and Japan are increasingly betting on the fact that optimism and confidence alone will solve the problems underlying the presently weak economic growth. On this matter I side with Buiter in thinking markets have gotten well ahead of economic realities, especially in the Euro Area periphery. Recent flare-ups highlight the ongoing undercapitalization of banks and the inability of fiscal policy to either reduce unemployment or meet given targets. Political fallout from recent scandals and a strengthening euro may reignite the EU crisis.

No comments:

Post a Comment