The Fed's Massive Accumulation of Treasuries Won't be Unwound

The Federal Reserve Will Need A 'Fairy Tale Ending' To Unwind Its Balance Sheet by Peter Tchir @ Money Game

I don’t see how the Fed announces anything that talks about taking down the balance sheet. Not now, and possibly not ever. The moment people get concerned, the market will start pricing in the unwind, no one will want to buy the long end of the curve and it will play havoc with rates.

Who in their right mind would buy 10 year treasuries when you know that the equivalent of multiple years of supply is being sold by the Fed along with the ones the Treasury department will need to sell. It isn’t like the Treasury department will be able to stop issuing bonds. They have to deal with rolls and frankly with ongoing deficits.

As a hedge fund, are you really going to “fight the fed” and buy 10 year bonds once you think they need to sell them? I don’t think so. More importantly, who will make a nice 10 year mortgage when the 10 year treasury is selling off?

That is the problem. The Fed has built up such a large portfolio, that the only likely way to exit it is through letting it mature. That at least takes the $2 trillion seller out of the market (remember, they are still in buying mode).

Due to the potential damage a sell off occurs, both in the cost of funds for the treasury, but more importantly in the knock on effect it has on other yield products, I would expect the Fed to defend any big move aggressively. Not only do they have the money to do it, but the float is small enough it may take far less than people think to defend the market.

Woj’s Thoughts - Six months ago I argued that an "Interest-On-Reserves Regime" Will Rule Monetary Policy For The Foreseeable Future because:

departing from this new regime will ensure that any future rate hikes be preempted by a reversal of the balance sheet expansion (or excess sale of Treasuries). Balance sheet contraction, through open market operations, could very well depress asset values and raise long-term interest rates. If this occurs, the Fed would be effectively causing a new crisis just as the economy is becoming increasingly stable.

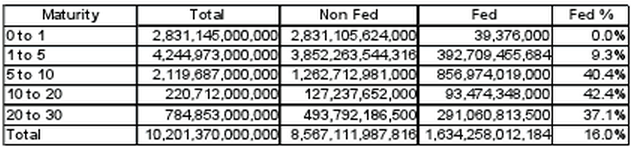

Tchir’s post breaks down the Federal Reserve’s current Treasury holdings, which amount to approximately 40 percent of outstanding supply in the 5 to 30 year maturity range. With the Federal Reserve now purchasing $45 billion of Treasuries per month, those percentages are set to grow rapidly in the coming year(s). Given the potential fallout from even signaling an end to current rounds of QE, I fail to see why future FOMC members would take the risk of actively reducing the monetary base when other options exists. This outlook for monetary policy is precisely why it’s so important to further understanding of the Permanent Floor.

No comments:

Post a Comment