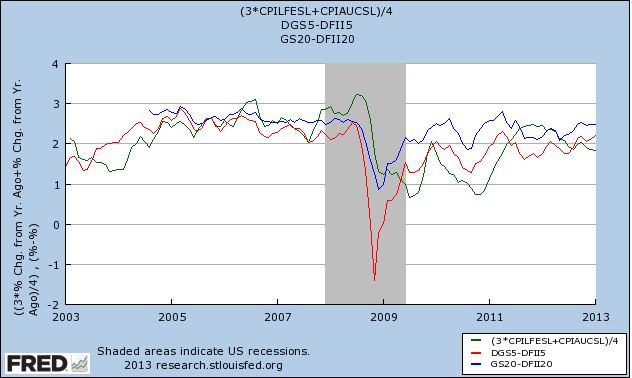

My claim is that expected inflation over the next 5 (and 10 and 20) years is very similar to actual inflation over the past year. I think the data generally fit the crudest most mechanical adaptive expectations hypothesis.

This would be interesting for two reasons.

First, the adaptive expectations hypothesis has been treated with utter contempt for roughly 4 decades. It is considered an example of the sort of thing which economists must utterly reject. The effort to replace it has lead to a lot of mildly interesting math and highly implausible assumptions.

Second, there is a huge and very vigorous discussion of forward guidance by the Fed Open Market (FOMC) Committee. It has been argued that even when the Federal Funds rate is essentially zero, the FOMC can stimulate the economy by causing higher expected inflation. It is generally agreed that the FOMC has been convinced by this argument. I think this implies that there should be anonalous increases in expected inflation on the dates when the FOMC began to try to cause higher expected inflation -- roughly the announcements of QE 1-4, operation twist and of forward guidance of how long it will keep the Federal Funds rate extremely low. An excellent fit of expected inflation using only lagged inflation creates serious difficulty for those who think the FOMC always could and finally has promoted higher expected inflation.

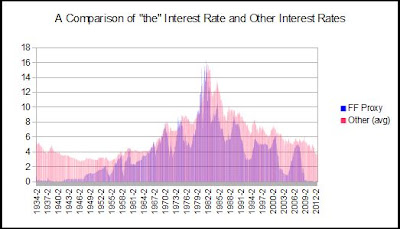

Woj’s Thoughts - This topic is reminiscent of a chain of posts nearly six months ago that began with JW Mason’s inquiry, Does the Fed Control Interest Rates? Jazzbumpa and Art Shipman chimed in with their own opinions, the latter providing this relevant chart on the path of interest rates over time:

Responding to the others’, my view was that:

Responding to the others’, my view was that:

market expectations of future Fed action are sticky. During the post-war period until about 1980, inflation was consistently rising despite mainstream economic views that suggested those conditions would not persist. Following a lengthy inter-war period of near rock-bottom interest rates, market participants were slow to adjust expectations to the actual height of interest rates that would occur before sustained disinflation began. Once disinflation began in the early 1980’s, market expectations were equally slow in recognizing how long disinflation could persist and therefore how low the Fed would ultimately take rates (and hold at zero).Returning to Robert’s claim, I suspect the recent strong correlation between the previous year’s actual inflation and inflation expectations for the next 5 or 20 years is partially due to the lengthy period of low inflation that came prior. In other words, if inflation were to start trending higher or lower over an elongated period, I predict inflation expectations would lag actual inflation while moving in the same direction. The adaptive inflation expectations hypothesis will therefore still hold, only more years of recent data will need to be incorporated into expectations formation. Validation of this hypothesis will deal a serious blow to the perception that Fed communications at the ZLB are an effective form of stimulus.

I think that adaptive expectations is a good proxy for what people are actually thinking when they make there decisions which affect the level of money and prices. But I also think that experience with an active CB provides more knowledge (stimulus) to individuals from which they will learn. So I'd be willing to go further and invoke the rational expectations model in periods and places that the CB has provided a pattern of behavior. I don't mean to say that people KNOW or understand or directly react to the CB. But they do act AS IF they know what incentives face a CB. They have pattern recognition which is forward looking (not just repeating at the same magnitudes and variance; which would be adaptive expectations). I always think of Argentina's Phillips curve. That screams Rational expectations to me.

ReplyDeleteWell the obvious follow up question is, what are the CB's incentives? IMO the primary goal is to ensure continuous, smooth functioning of the payments system. Previously inflation appeared to be the secondary priority, now with the Evans' rule that distinction goes to a combination of inflation and employment. The trouble is that as much as the Fed may want to generate higher inflation and employment, it simply lacks the tools necessary to create those outcomes. Therefore individuals adjusting expectations based on the Fed's actions may have been rational, but they were also wrong.

DeleteThinking back to the period before the crisis, there is reasonable evidence that the Fed was not only a passive participant in terms of supplying reserves but also adjusting interest rates. If you look at the other links in this post, that was the primary discussion. If the Fed is reacting to markets, then people acting as if they know the Fed's actions are also acting as if they know the markets actions. In that case, however, I fail to see what added value knowledge of the Fed provides.

As for Argnetina's Phillips curve, I'm not sure which period you're referring to or how that fits this discussion exactly. Could you please elaborate a bit more?

There is a huge literature on expectations, not only of inflation, but also interest rates, default risk, exchange rates, etc., and the hypothesis of rational expectations is overwhelmingly rejected. It really won't do to just go on asserting a priori.

DeleteI think Robert is right here. I've been looking at interest rate expectations, and the evidence is pretty overwhelming that expectations of future interest rates are really just equal to recent interest rates. I don't think there's any evidence that interest rate expectations incorporate a trend at all, even though the actual trajectory of interest rates seems to include decades-long trends. I suspect inflation expectations are similar.

ReplyDeleteIn any case, I certainly agree that forward guidance has no effect.

Woj,

ReplyDeleteBeing the novice, non-economist, I'll ask the stupid question: If the market sets the Fed funds rate, what happens if the Fed raises the discount rate? Right now the spread is about 50 basis points, right? Well, what if the Fed raised the discount rate another 100-150 basis points? Would that send a signal to the market, and in effect raise the Fed funds rate?

Discount window borrowing is essentially zero at this point, so raising this rate should have a minimal effect, if any. The discount window effectively sets a ceiling on the price for reserves since banks will never pay a higher rate on the interbank market when the Fed will provide unlimited reserves through the discount window (ignoring any negative stigma associated). When the financial crisis first struck, borrowing at the discount window shot up to ~$400 billion as banks were unwilling to lend reserves for other collateral. This effectively raised the cost of base money for many banks and was a de facto tightening of monetary policy.

DeleteUnder the permanent floor system, the banking system is flowing with excess reserves so the IOR rate becomes not only the floor but the effective rate of base money. It therefore seems very unlikely that banks would need to access the discount window in any meaningful size. If that's true, then raising the rate will only alter lending decisions for those banks presumably weak enough to not have collateral to borrow funds in the interbank market.

Packers And Movers Bangalore to Indore

ReplyDeletePackers And Movers Bangalore to Madurai

Packers And Movers Bangalore to Cochin

Packers And Movers Bangalore to Ranchi

Packers And Movers Bangalore to Surat

Packers And Movers Bangalore to Raipur

Packers And Movers Bangalore to Thane

Packers And Movers Bangalore to Srinagar

Packers And Movers Bangalore to Vishakhapatnam

Hey, Wow all the posts are very informative for the people who visit this site. Good work! We also have a Blog. Please feel free to visit our site. Thank you for sharing.

ReplyDeletePlease visit our website : Packers And Movers Mumbai

Packers And Movers Mumbai to Noida

Packers And Movers Mumbai to Guntur

Packers And Movers Mumbai to Muzaffarpur

I could not have closed on my first home without Mr, Benjamin Lee ! Benjamin and his team went above and beyond for me on this transaction. He handled my very tight turn around time with ease and was always available for me when I had questions (and I had plenty), even when he was away from the office, which I greatly appreciated! He and his team handled many last-minute scrambles with the seller and worked tirelessly to make sure that I could close before my lease (and my down payment assistance, for that matter) expired. Mr Benjamin is an incredibly knowledgeable Loan Officer, courteous, and patient. I went through a couple offers on properties before my final purchase and Benjamin was there to help with each one, often coordinating with my agent behind the scenes. I felt supported throughout the entire process. Thanks to Benjamin and the tireless efforts of his team, I am now a proud homeowner! I would encourage you to consider Benjamin Briel Lee for any kind of loan.Mr, Benjamin Lee Contact informations.via WhatsApp +1-989-394-3740 Email- 247officedept@gmail.com.

ReplyDeleteCheck the latest govt Jobs 2025 here at <a href="https://www.egovjob.com/latest-jobs/”>Egovjob</a>

ReplyDeleteGreat post! For anyone looking for the latest job online form, check out this Egovjob.

ReplyDelete