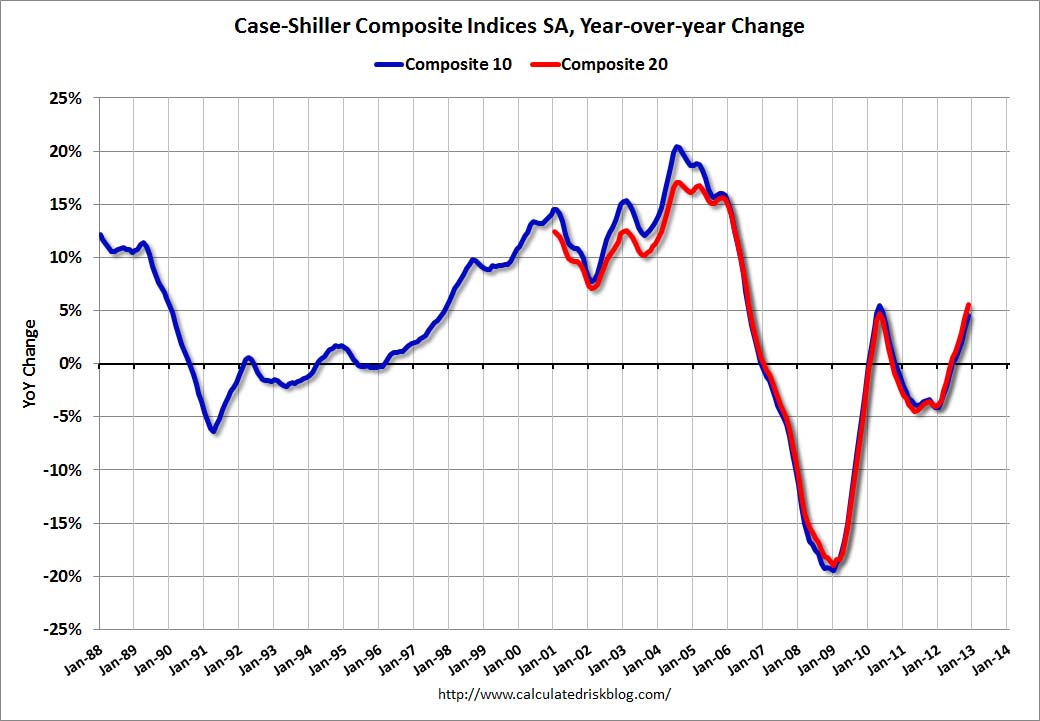

When deciding whether or not to purchase a home, there are certainly a whole host of factors to consider that were not discussed here (family, job security, income, savings/debt, location, etc). The purpose is to provide an alternative perspective to the seemingly common perception that now is the best time to buy and those who fail to act will miss a great opportunity. While I don’t rule out that possibility, I believe the outlook for home prices and mortgage rates suggests this window of opportunity will remain open for a few years. In fact, those who wait may be rewarded with lower mortgage rates and more house for their money. There is no rush to buy a home!Now with the benefit of hindsight, my judgment appears to have held up relatively well. Although house prices have risen approximately 6 percent in the past year:

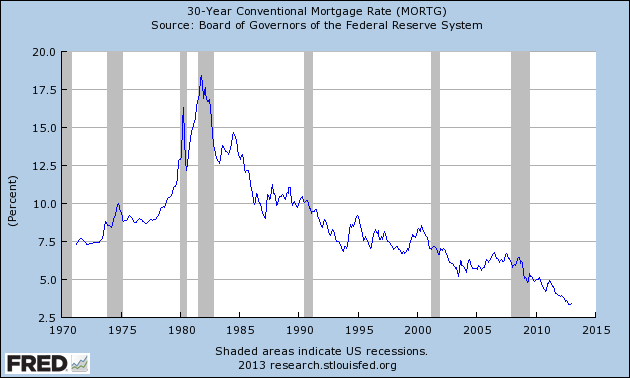

30-year fixed rate mortgages touched a new low of 3.3%:

With 2013 only a month old, conversation among friends and family about buying new homes has picked up once again. Oddly enough, the substantial rise in prices over the past year is stoking demand for housing. (I say oddly because basic economics suggests demand should decrease when prices rise) However, before offering my views on future house prices, let me say a few words about mortgage rates.

With 2013 only a month old, conversation among friends and family about buying new homes has picked up once again. Oddly enough, the substantial rise in prices over the past year is stoking demand for housing. (I say oddly because basic economics suggests demand should decrease when prices rise) However, before offering my views on future house prices, let me say a few words about mortgage rates. Over the past few months the FOMC has initiated QE3 (QEternity) and QE4, which involves purchasing $40 billion of Agency-MBS and $45 billion of Treasuries per month. Despite jubilant asset markets, inflation (core-PCE) and GDP growth remain well below 2 percent. This failure to stimulate real growth will likely lead the FOMC to extend its pledge of maintaining interest rates near 0 until at least 2016. Based on this combination of QE, ZIRP, low inflation, and stagnating growth, the chances of mortgage rates rising back above 4 percent anytime soon seems very limited.

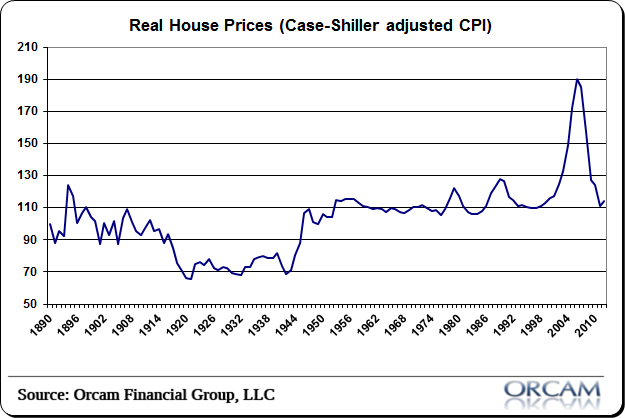

Returning to the future direction of house prices, I remain skeptical that household balance sheets have been sufficiently repaired to permit a new debt-led boom. One of the better resources for housing market insights, Dr. Housing Bubble has highlighted the recent surge in investment demand. Meanwhile, Diana Olick discusses reports that Americans are tapping their homes for cash again. Clearly aspects of the previous bubble are returning, which makes it tough to rule out further gains in the short-term. That being said, US residential real estate just isn’t a great investment in real terms and here is Robert Shiller explaining why:

“Housing is traditionally is not viewed as a great investment. It takes maintenance, it depreciates, it goes out of style. All of those are problems. And there’s technical progress in housing. So, the new ones are better….So, why was it considered an investment? That was a fad. That was an idea that took hold in the early 2000′s. And I don’t expect it to come back. Not with the same force. So people might just decide, ‘yeah, I’ll diversify my portfolio. I’ll live in a rental.’ That is a very sensible thing for many people to do.

…From 1890 to 1990 the appreciation in US housing was just about zero. That amazes people, but it shouldn’t be so amazing because the cost of construction and labor has been going down.

…They’re not really an investment vehicle unless you want it for your personal reasons.”If you want more proof, here is the chart Shiller is referencing:

My recommendation therefore remains basically the same as last year. Housing prices and mortgage rates may have bottomed, but the odds of either rising substantially in the next couple years remains small. Ultimately you should buy a house that you want to live in, not that you hope will be a good investment. If you plan on buying, just remember, there is no rush to buy a home!

Great article! Thank you very much for the insight.

ReplyDelete