I saw this headline over at Calculated Risk regarding the new “monetary policy” in Japan:

And from the Japan Times: Japan’s economic minister wants Nikkei to surge 17% to 13,000 by MarchEconomic and fiscal policy minister Akira Amari said Saturday the government will step up economic recovery efforts so that the benchmark Nikkei index jumps an additional 17 percent to 13,000 points by the end of March.“It will be important to show our mettle and see the Nikkei reach the 13,000 mark by the end of the fiscal year (March 31),” Amari said in a speech.The Nikkei 225 stock average, which last week climbed to its highest level since September 2008, finished at 11,153.16 on Friday.“We want to continue taking (new) steps to help stock prices rise” further, Amari stressed …

…

Yes, the Bank of Japan might create some real wealth (for some market participants) in the near-term and might thereby make Japan appear better off than they really are, but there’s absolutely no underlying fundamental change in the corporations that make up this index that should lead one to believe that these price changes are justified. And when the Ponzi scheme is exposed the market collapses thereby destroying wealth for all the current participants leaving us right back where we started.

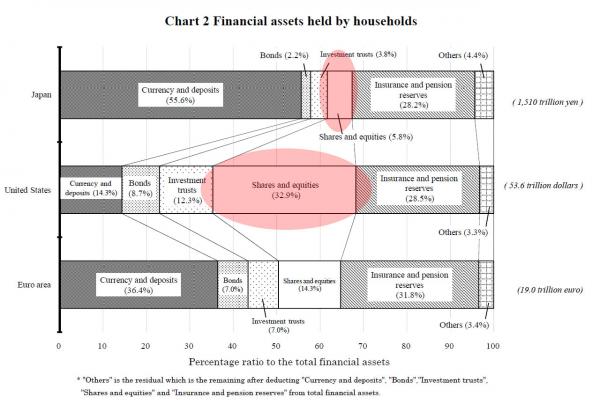

This is ponzi based monetary policy. It’s based on a false understanding of market dynamics, a false understanding of real wealth, and it’s very likely to cause disequilibrium in the long-term.Woj’s Thoughts - While these comments made investors giddy, as expected, I can’t help but feeling that the continued onslaught of “open mouth” operations from Japanese officials is masking their deficient understanding of modern monetary economics. If wealth effects from higher stock prices are largely irrelevant in the U.S., what are the odds the effect will be greater in Japan where equities play a much smaller role in household portfolios?

As Niels Jensen makes clear in his most recent investor letter, the Nikkei’s recent surge combined with a plunging Yen suggests the pressures in both markets are arising primarily from foreign investors.

Prior to PM Abe taking office I was skeptical of fiscal and monetary policies actually being enacted that would materially raise either inflation or real GDP growth (effectively NGDP). Since then a minor fiscal stimulus package was announced along with a higher inflation target and commitment to future QE. Looking beyond the initial market optimism, none of these measures will actually generate the economic results to match the widespread wishful thinking. Fourth quarter NGDP was just recently announced at zero percent and real GDP fell for the third consecutive quarter. Unless further drastic policy actions are taken, I suspect future quarters will more closely resemble the current quarter than the hoped for 4% NGDP growth.

(Note: Cullen describes Japan’s theoretical new policy as a Ponzi scheme, but I think that terminology may be incorrect in this situation. Since the Bank of Japan (BoJ) can create an unlimited supply of reserves, it does not require any new lending to continually maintain any price for the Nikkei it chooses. The scariest outcome is not that the scheme would collapse, but that the BoJ would end up controlling all currently public corporations.

To be clear, I doubt that outcome would happen in practice. The more likely endgame is that the policy becomes politically unacceptable and then the BoJ retracting its price target leads to a spectacular (ponzi-esque) crash.)

No comments:

Post a Comment