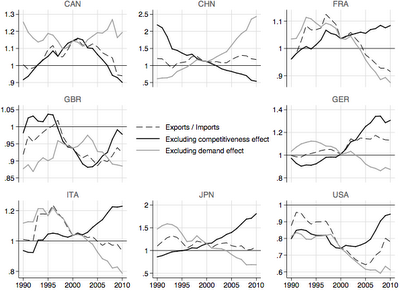

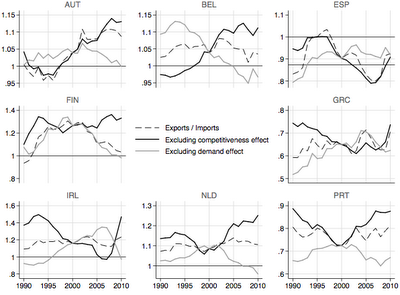

The heart of the paper is an exercise in historical accounting, decomposing changes in trade ratios into m*/mand D*/D. We can think of these as counterfactual exercises: How would trade look if growth rates were all equal, and each county's distribution of spending across countries evolved as it did historically; and how would trade look if each country had had a constant distribution of spending across countries, and growth rates were what they were historically? The second question is roughly equivalent to: How much of the change in trade flows could we predict if we knew expenditure growth rates for each country and nothing else?

The key results are in the figure below. Look particularly at Germany, in the middle right of the first panel:

The dotted line is the actual ratio of exports to imports. Since Germany has recently had a trade surplus, the line lies above one -- over the past decade, German exports have exceed German imports by about 10 percent. The dark black line is the counterfactual ratio if the division of each county's expenditures among various countries' goods had remained fixed at their average level over the whole period. When the dark black line is falling, that indicates a country growing more rapidly than the countries it exports to; with the share of expenditure on imports fixed, higher income means more imports and a trade balance moving toward deficit. Similarly, when the black line is rising, that indicates a country's total expenditure growing more slowly than expenditure its export markets, as was the case for Germany from the early 1990s until 2008. The light gray line is the other counterfactual -- the path trade would have followed if all countries had grown at an equal rate, so that trade depended only on changes in competitiveness. When the dotted line and the heavy black line move more or less together, we can say that shifts in trade are mostly a matter of aggregate demand; when the dotted line and the gray line move together, mostly a matter of competitiveness (which, again, includes all factors that cause people to shift expenditure between different countries' goods, including but not limited to exchange rates.)Woj’s Thoughts - If correct, this explanation for global trade imbalances would certainly throw a wrench in standard, mainstream theories that assume prices and exchange rates respond to alleviate any imbalances. Clearly greater relative income growth should lead to larger imports relative to exports. Using a sectoral balances approach, the question is why doesn’t the boost to aggregate demand from rising trade surpluses alter prices and income in a manner that creates convergence? I certainly don’t expect the changes to happen quickly, but remain of the view that some institutional factors (e.g. tax policy, financial regulations) likely encourage diverging prices and incomes.

2) Hoenig: A Better Alternative to Basel Capital Rules by Thomas Hoenig via The Big Picture

Basel III is intended to be a significant improvement over earlier rules. It does attempt to increase capital, but it does so using highly complex modeling tools that rely on a set of subjective, simplifying assumptions to align a firm’s capital and risk profiles. This promises precision far beyond what can be achieved for a system as complex and varied as that of U.S. banking. It relies on central planners’ determination of risks, which creates its own adverse incentives for banks making asset choices.

3) S&P: Australia is Spain in waiting by Houses and Holes @ MacroBusiness

Australia must find a Budget surplus before 2014 or it will lose its AAA rating, according Kyran Curry, S&P sovereign analyst via the AFR:

“If there’s a sustained delay in returning the balance to surplus, as the economy gathers momentum and as people start spending again, as the import demand picks up and current account blows out, we might not see the government’s fiscal position as being strong enough to offset weaknesses on the external side and that’s what worries us…Australia’s already, as we see it, got some credit metrics that are right off the scale when it comes to assessing Australia’s external position…It’s got high levels of external liabilities, it’s got very weak external liquidity and that basically means the banks are very highly indebted compared to their peers…For us, we look to Spain, which was Australia’s closest peer four or five years ago in terms of having a very strong fiscal position, very similar to what Australia has at the moment, its external position was weaker, like Australia’s, and it got routed very quickly…The government needed to provide support to the banks, it had to shore up growth in the economy and its debt levels more than doubled…We can see that happening in Australia’s case.”Woj’s Thoughts - Contrary to popular perception and especially the Market Monetarist crowd, I’ve been arguing that Australia is facing serious headwinds that will end its impressive growth streak. In this context, Spain offers a reasonable comparison considering its high levels of private debt, housing bubble and high level of external liabilities prior to the current crisis. Having a sovereign currency permits Australia more scope in terms of policy responses, however the current government seems keen on following Europe’s approach. If the Australian government attempts to “find a Budget surplus before 2014,” it may keep its AAA rating while almost certainly exacerbating the downward spiral.

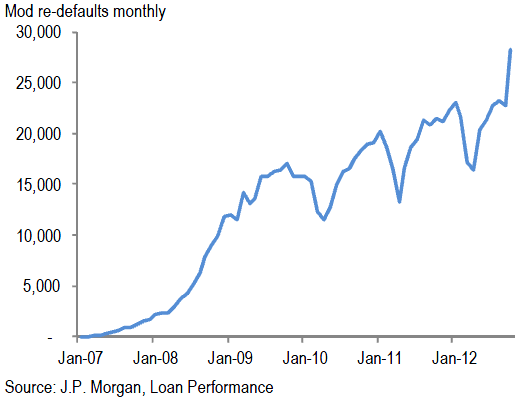

4) Borrowers with modified mortgages re-default as homes re-enter shadow inventory by Walter Kurtz @ Sober Look

We are therefore seeing a sharp rise in re-defaults from modified mortgages.

This is telling us that mortgage modification programs have not been very successful, as the probability of re-default rises. By modifying mortgages, banks in many cases are simply kicking the can down the road - and now some are writing down these mortgages (which may be what is driving the higher charge-off numbers). We are therefore seeing an increase in delinquencies, but mostly among modified mortgages and concentrated in sub-prime portfolios.Woj’s Thoughts - Bad news for banks and the government. Mortgage modifications were simply not enough for many homeowners who remain underwater and without the requisite income and/or savings to seemingly ever repay the entire loan. If this new wave of re-defaults persists, as JP Morgan expects, housing prices and bank earnings may return to a downward trend.

5) China's Economic Growth: A Different Storyline by Timothy Taylor @ Conversable Economist

When I chat with people about China's economic growth, I often hear a story that goes like this: The main driver's behind China's growth is that it uses a combination of cheap labor and an undervalued exchange rate to create huge trade surpluses. The most recent issue of my own Journal of Economic Perspectives includes a five-paper symposium on China's growth, and they make a compelling case that this received wisdom about China's growth is more wrong than right.

For example, start with the claim that China's economic growth has been driven by huge trade surpluses. China's major economic reforms started around 1978, and rapid growth took off not long after that. But China's balance of trade was essentially in balance until the early 2000s, and only then did it take off. Here's a figure generated using the ever-useful FRED website from the St. Louis Fed.Woj’s Thoughts - I always have a soft spot for arguments, backed by data, that undermine the mainstream opinion. Although I continue to side with Michael Pettis on the forthcoming rapid slowdown in China’s GDP growth, I agree that growth will persist and lead to a much higher standard of living in the future.