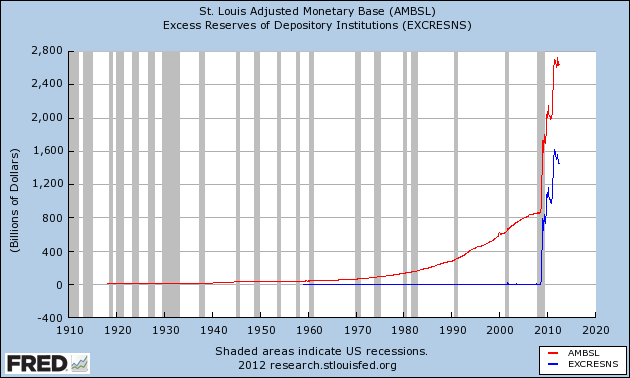

To provide a quick gist of the discussion during these morning panels and the detrimental effects of excessive private debt, here are a few snippets from Michael Hudson’s prepared remarks:

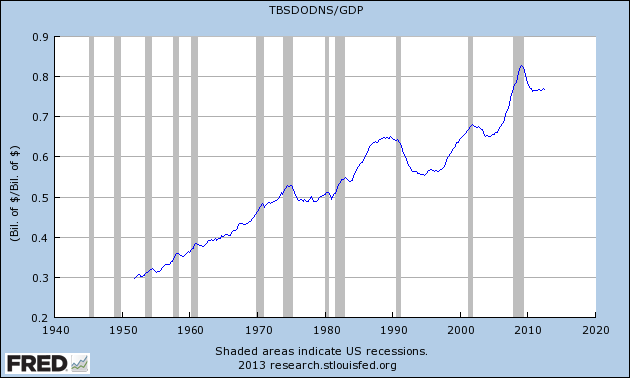

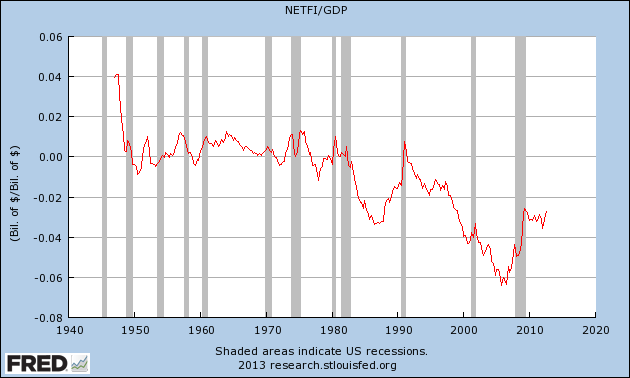

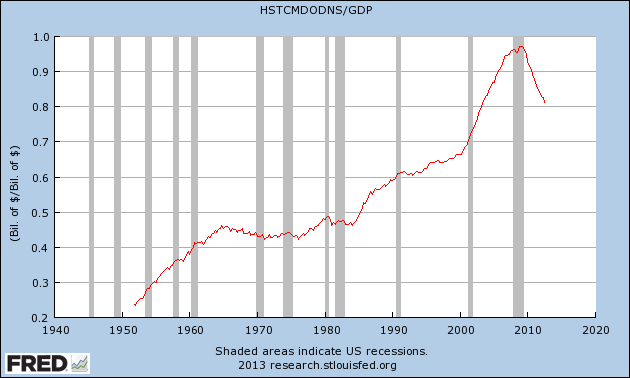

The result of the private-sector debt overhang is a self-feeding spiral of debt deflation. Revenue earmarked to pay bankers is not available to spend on goods and services. Lower consumer spending is a major reason why firms are not investing in tangible capital to produce more output. Markets shrink, shopping malls close down, and empty stores are appearing for rent on major shopping streets from New York City to London.

Slowing employment is causing a state and local budget squeeze. Something has to give – and it is largely pension plans, infrastructure spending and social programs.

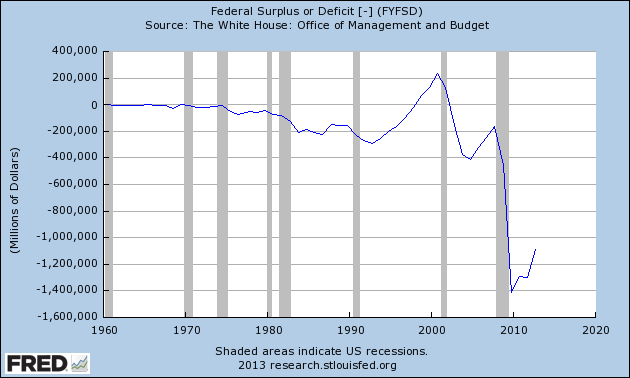

However, the one kind of debt we are not worried about is government debt. That’s because governments have little problem paying it. They do not need to balance their budget with tax revenue, because their central bank can simply print the money. On balance, the overall public debt rarely needs to be paid down. As Adam Smith noted in The Wealth of Nations, no government in history ever has paid off its public debt.

…

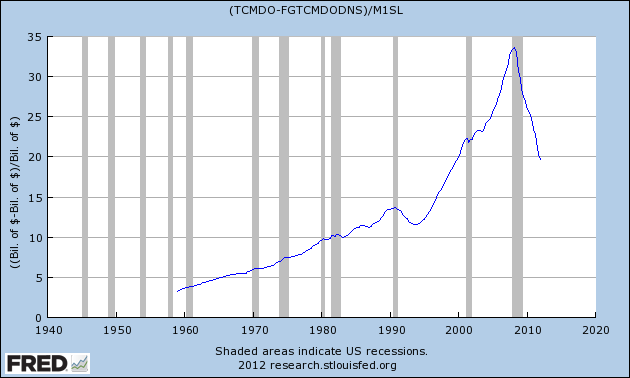

The policy lesson for today is that to avoid debt deflation, falling markets and unemployment, the economy needs to be revived. The way to do this is what was called for and indeed promised four years ago: a write-down of debts in keeping with the ability to pay.

Once this debt overhead is addressed, tax reform is needed to prevent a debt bubble from recurring. A tax system that favors debt financing rather than equity, and that favors asset-price “capital” gains and windfall gains over wages and industrial profits earned by producing tangible output, has been largely to blame. Also needing reform is tax favoritism for the offshore fictitious accounting that has become increasingly unrealistic in recent years.

Unless government fiscal policy addresses these issues, the U.S. economy will face the same kind of debt-deflation pressures and fiscal austerity that is now tearing the eurozone apart.As the only two economists in attendance who predicted the financial crisis and subsequent stagnation, Hudson and Keen’s panel stood out in offering practical policy responses that will not further increase wealth inequality or the financial sector’s profits/influence:

Good Debt, Bad Debt & Real Options for Economic Growth from The Atlantic on FORA.tv

A brief detour from discussion of the conference, Professor Steve Keen has been working hard on building a computer program for building & visually simulating dynamic, monetary economics models: http://kck.st/XhKtdX

There are only 2 days left to show your support for the project on Kickstarter and help reach the secondary funding goal of $100,000. Please check out the Kickstarter page for more information and consider making a pledge to improve the future of economics:

MINSKY: Reforming economics with visual monetary modeling

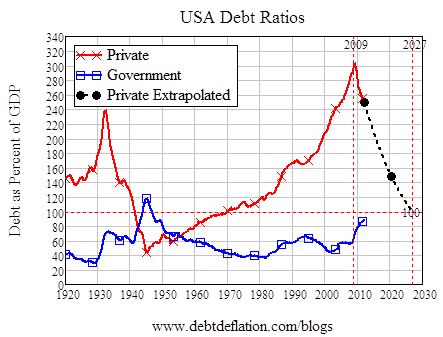

Returning to the conference and giving credit where its due, The Atlantic has been working with and, in the afternoon session, featured Richard Vague’s work on “How to Deal With America’s Private Sector Debt Challenge”:

How to Deal with America's Private Sector Debt Challenge from The Atlantic on FORA.tv

Slides from the presentation and a host of other fantastic data can be found at the Debt Economics website.

Lastly I’ll recommend watching the first panel of the day which included not only Yves Smith but deficit doves Paul McCulley and Robert Kuttner:

Robert Kuttner & Others Debate U.S.'s Addiction to Debt from The Atlantic on FORA.tv

(Unfortunately the moderator was particularly determined to focus the conversation on the Ryan budget and public debt issues).

While I don’t know how many conference attendees will have been swayed by the presentations above, I think it’s a step in the right direction that these discussions are at least taking place within the mainstream community.

(Note: Although I was already a big supporter of Keen, Hudson, and Smith’s work, I should note that all three were incredibly gracious in conversation when I approached them. Separately, I apologize for the lack of blogging during the past couple weeks. My last midterm is Monday night and I hope to return to more frequent shortly thereafter.)