...is from Irving Fisher’s remarkable work, The Debt-Deflation Theory of Great Depressions:

“Thus over-investment and over-speculation are often important; but they would have far less serious results were they not conducted with borrowed money. That is, over-indebtedness may lend importance to over-investment or to over-speculation. The same is true as to over-confidence. I fancy that over-confidence seldom does any great harm except when, as, and if, it beguiles its victims into debt.”

The first quarter of 2012 has officially come to an end with the S&P 500 logging its best quarterly performance since 1998. For the first three months of the year, the index gained an impressive 12%. With fears about a European debt crisis subsiding, confidence among investors that a new cyclical, and possibly secular, bull market is beginning is rising quickly. Each time the market tries to sell-off even 1% in a day, buyers jump in and reverse the trend. Analysts are also ratcheting up year-end expectations to match the intense rally currently taking place.This combination of positive factors is seemingly creating an environment where investors once again believe they can’t lose. Central banks across the globe, most notably the Federal Reserve, have made clear the desire to push stock markets higher. Many investors believe the Fed will still engage in QE3 in the coming months, irregardless of high oil prices or rising inflation expectations. Overall there appears to be a strong level of complacency in global markets.Nearly 80 years ago, Irving Fisher recognized the importance of private debt levels in exacerbating the inflationary, than deflationary effects of over-investment and over-speculation. As over-confidence once again stems from a perpetually rising stock market, investors are becoming more comfortable with increasing their level of debt. As the following chart shows, margin debt (blue lines) is following the stock market (red line) higher.

Source: (The Big Picture)The last two market peaks, in 2007 and 2011, corresponded with margin debt rising above the $300 billion mark. Data for March, which has yet to be released, may show margin debt again eclipsing that level. Whether or not this signals another market top, the lesson of increasing debt is clear. When markets eventually turn, this borrowed money will accelerate moves to the downside.

Source: (The Big Picture)The last two market peaks, in 2007 and 2011, corresponded with margin debt rising above the $300 billion mark. Data for March, which has yet to be released, may show margin debt again eclipsing that level. Whether or not this signals another market top, the lesson of increasing debt is clear. When markets eventually turn, this borrowed money will accelerate moves to the downside.

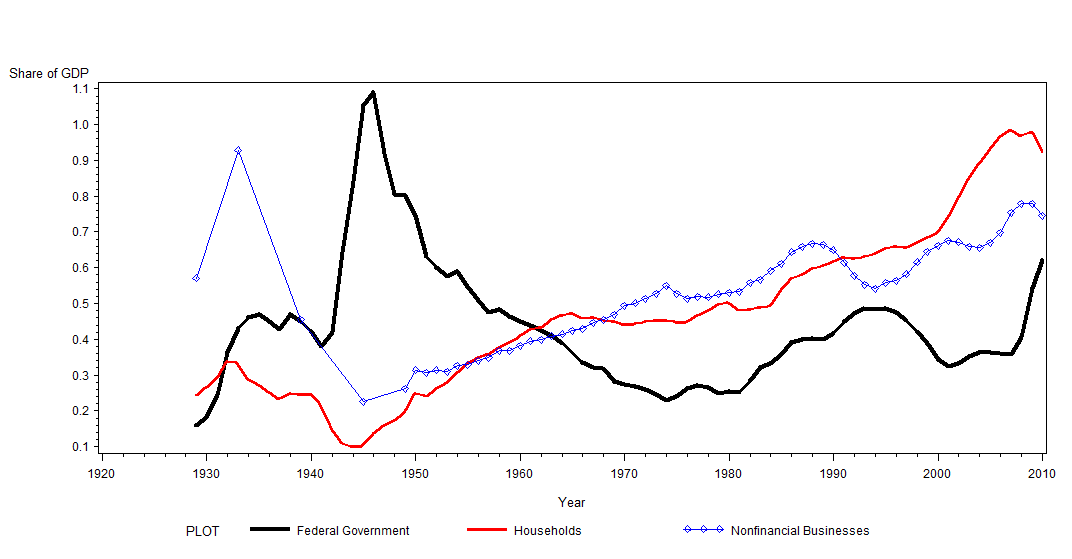

Over the past few years, public policy has relentlessly attempted to ensure the solvency and profitability of the financial sector, namely the largest financial institutions. Lost in these efforts is any recognition that the Great Recession was primarily due to a highly indebted household sector being pressured to reduce leverage. As shown in the graph below (from Fisher Dynamics in Household Debt: The Case of the United States, 1929-2011), household debt as a percentage of GDP increased from approximately 10% in 1945 to nearly 100% by 2007.

As an avid follower of new economic work being done in Post-Keynesianism, Modern Monetary Theory (MMT) and Modern Monetary Realism (MMR), I’ve often been perplexed by apparent inconsistencies in discussions regarding saving and leverage. My confusion stemmed, in part, from the notion that households are capable of saving and increasing leverage (debt as a share of GDP) at the same time. If you’re a bit confused at this point, don’t worry, I’ll explain the situation more simply in a moment.

Before moving on, it’s important to recognize that economic terminology often does not fit with typical usage of every day words. Here are some important economic terms to understand going forward:

Saving - The difference between disposable income and consumption.

Disposable Income - Income minus taxes.

Consumption - The amount spent on non-durable goods (e.g. food, clothing) plus the amount spent on durable goods (e.g. autos) spread over the item’s life span. (Note: Purchasing a home is an investment, for which an imputed rent is counted as consumption.)

Using this definition of saving, it becomes clear that households can maintain a positive savings rate yet still be net borrowers, as long as that borrowing goes towards investments. Ramanan, a horizontalist, recently explained this concept in a wonderful post on Saving Net Of Investment [Updated]. From this perspective, the frequent comment that households must increase saving to reduce leverage is clearly false. The rise in household debt during the post-WWII period is apparently based on net borrowings, not the private savings rate.

This new found understanding has proved short-lived after reading the following Guest Post by JW Mason: The Dynamics of Household Debt over at Rortybomb. A new working paper finds

“that changes in borrowing behavior has played a smaller role in the growth of household leverage than is widely believed. Rather, most of the increase can be explained in terms of “Fisher dynamics” — the mechanical result of higher interest rates and lower inflation after 1980.”

Put in simpler terms, interest rates on household debt since 1980 have been consistently higher than income growth. Under these conditions, even without increasing borrowing, household leverage will increase. Over the past few years, household leverage has been decreasing largely due to debt write-downs. With this process slowing, the scenario mentioned above is likely to return. Even though interest rates remain at or near historical lows, income growth has been practically stagnant. Without a drastic change in these variables, the large burden of household debt is likely to continue suppressing consumer demand well in to the future. Attempts by households to increase saving may inadvertently decrease income, exaggerating the problem. Simply put, significant debt write-downs (a modern day debt-jubilee) may be necessary to restore the household sector to a stronger, more stable, financial position.