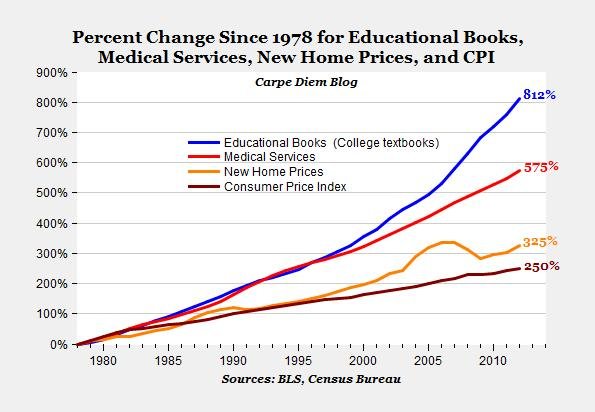

1) The College Textbook Bubble Is Out Of Control by Sam Ro @ Money Game

Here's the insane chart:

Woj’s Thoughts - Why are textbooks so expensive today? We all know that student loans are rising exponentially to pay for tuition. Is it possible those loans are also subsidizing textbook sales? It’s doubtful that quality has increased that dramatically in the past 40 years and production costs are certainly lower. I suspect there is some institutional arrangement creating the surge higher, but unsure of specifically what that might be. Any suggestions?

2) The Folly of Obsessing over Marginal Tax Rates, by Garett Jones @ EconLog

It's often wise to pay more attention to marginal tax rates than to average tax rates. If you can make your first $100 tax free but the 101st dollar is taxed at a marginal rate of 99% you'll probably decide to earn $100 at most.

But what is marginal? When it comes to career choices or the state you'll live in or whether to have an extra child the marginal decision is very big, and a rational person will base that decision mostly on the average long run costs and benefits. In cases like this, the official marginal tax rate won't matter nearly as much as the long run average tax rate.

3) A Free-Market Monetary System by Friedrich A. Hayek @ Ludwig von Mises Institute

I think it is very urgent that it become rapidly understood that there is no justification in history for the existing position of a government monopoly of issuing money. It has never been proposed on the ground that government will give us better money than anybody else could. It has always, since the privilege of issuing money was first explicitly represented as a Royal prerogative, been advocated because the power to issue money was essential for the finance of the government-not in order to give us good money, but in order to give to government access to the tap where it can draw the money it needs by manufacturing it. That, ladies and gentlemen, is not a method by which we can hope ever to get good money. To put it into the hands of an institution which is protected against competition, which can force us to accept the money, which is subject to incessant political pressure, such an authority will not ever again give us good money.

Woj’s Thoughts - Warren Mosler has often suggested researching the “Currency as a Public Monopoly” for my dissertation. While I’m not entirely sold on that project, at least yet, I was bit surprised to find this speech by Hayek discussing his own research on “a government monopoly of issuing money.” Although Mosler and Hayek almost certainly hold different views about the benefits and costs of such a monopoly, the potential of researching both perspectives piqued my interest. Maybe I will do some preliminary research on the subject and see where it leads.

The other night, a counterpart in my PhD program claimed that Post-Keynesian economists generally deny any truth behind the Austrian views on heterogeneous capital. While others are free to correct to this statement, I suggested that while modern money approaches often don’t discuss capital as a central theme, the two theories need not be contradictory. Ryan Murphy’s argument that It does matter how new money is injected, but that’s probably bad terminology, offers a chance to briefly discuss my thinking on the subject (my emphasis):

The idea that it matters how new money is injected relates to the way in which money “hits” the markets. For the “traditional” story to apply, the price of time -the interest rate- needs to move before other prices move. If it “hits” consumption goods (or some other vector of goods) first, the traditional ABCT story doesn’t apply, though something similar in substance might.

The simplest way to think about this is with Hayekian triangles. It’s a fairly simple question: can monetary policy disrupt the shape of the triangle in the way Garrison described via interest rates? I don’t see why this would be controversial. Some industries (and economic decisions generally) are more sensitive to interest rate changes than others. If you were at monetary equilibrium and you print money in such a way that causes interest rates to fall, then more resources get drawn into those industries than elsewhere. That is almost true by definition. If you assume heterogeneous interest rate sensitivity and that monetary policy can affect interest rates, then you get heterogeneous real effects.

Ryan’s post is a reaction to one by Scott Sumner arguing that it makes very little difference how new money is injected into the economy. The second paragraph above presents an Austrian explanation that seems readily apparent through recent experience. A decade ago, expectations that short-term interest rates would remain relatively low for quite some time helped bring down long-term interest rates. The housing sector, particularly sensitive to long-term rates, saw increasing growth and speculation. More resources were drawn to the sector than elsewhere, fueling a spectacular bubble. When the bubble burst, the economy experienced a real shock to growth.

These effects from monetary policy are only one part of the story. Looking back at Ryan’s first paragraph above, a modern money perspective (is this better than saying Post-Keynesian?) may provide the “something similar in substance”. This view argues that fiscal policy is partially responsible for injecting money into the economy (“inside” money from private banks being the main source). Depending on the distribution, prices in certain industries may adjust before changes in interest rates. These industries will likely attract more resources temporarily due to changes in expected future demand. When the government reduces or stops supporting those industries, revealing the temporary nature of the demand, prices will tend to fall. In this light, fiscal policy that alters the money supply also creates real effects due to the misallocation of capital.

Starting from either approach, it seems clear that money is non-neutral. Given this agreement, I see no reason why modern money and heterogeneous capital perspectives need be incompatible. Hopefully others can shed some further light on this debate.

(Note: Two bloggers that often combine an Austrian and modern money approach (from whom I’ve learned a great deal) are Edward Harrison of Credit Writedowns and John Carney at CNBC’s NetNet.)

Related posts:

The Fallacy of Monetary Neutrality

Fighting for Endogenous Money on Two Fronts

Hayekian Limits of Knowledge in a Post-Keynesian World