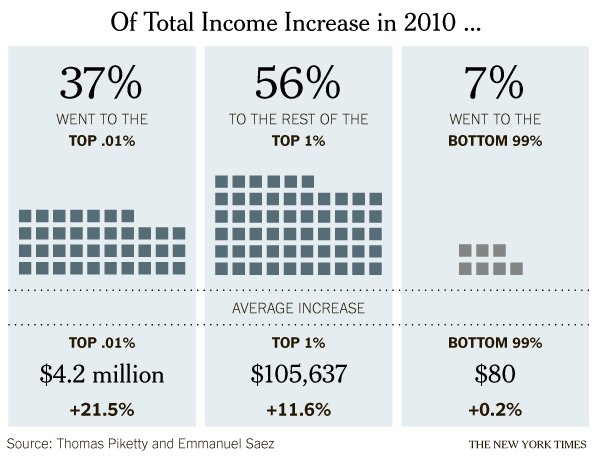

Philip Pilkington: The New Monetarism Part I – The British Experience

The monetarist experiment proved disastrous. The Bank of England failed completely to control the money supply and succeeded only in causing interest rates to spiral out of control. This threw the economy into a deep recession. Between the last quarter of 1978 and the last quarter of 1980 the M3 measure of the money supply – the target of the monetarists – rose by some 32.8%; this was significantly faster than in the years before the targets had been initiated. Meanwhile unemployment skyrocketed and businesses shut their doors.

…

Note the resemblance to today’s QE program. Many in the markets and the media have succumbed to a sort of ‘QE fatigue’ as it is obvious that the policy has not produced the desired effect. Nevertheless, QE continues to live on as a sort of undead policy tool. A great deal of the reason for this is that those engaged in the markets can still trade on QE. For example, if another round of QE is announced by a central bank an investor can short the currency of that country, buy their government bond or throw money at the stock market. The brief increase or decrease, generated mostly by self-fulfilling expectations, can then give their portfolios a boost. Economists and commentators also cling to QE because it gives them something to talk about which they can use to enhance their prestige – this even though QE, stripped of its aura, is a straightforward asset swap program that a child could understand.Philip Pilkington: The New Monetarism Part II – Holes in the Theory

Friedman was convinced that if he could prove that Keynes was wrong by showing that the velocity of money was relatively fixed and that there was thus a fairly simple mechanical relationship between the money supply and national income, the Keynesian theory would largely fall apart. If Friedman was correct he would also be able to explain inflation as simply being due to the central bank allowing too much money flow into the economy relative to the size of that economy and that all they had to do was target a given money supply to bring the inflation under control.

...

So, what was wrong with Friedman’s basic theory? Well, first of all the correlations he thought he found were not the same across time and space. If the data for many countries is compared across time we see strong fluctuations in the velocity of money. Indeed, even within single countries the velocity of money fluctuates quite aggressively in line with overall economic growth. Here, for example, is the velocity of the M2 money supply in the US charted together with the employment-population ratio – an indicator of economic health that is used to determine the ability of the economy to produce jobs:

Clearly the velocity of the M2 is not at all constant and moves in rough correlation with the employment-population ratio and, hence, with the health of the economy. So, Friedman was wrong on even the simplest measure. The velocity of money does, in fact, vary over time.

Does this mean that Keynes was correct and large-scale unemployment could not be cured by monetary stimulus due to a falling velocity? No, not really. Keynes’ idea that the velocity of money would move together with the level of economic activity (and the interest rate) was simply a modification of the old quantity theory of money. Thus all Friedman had to do was show a constant velocity and he could debunk Keynes. But in actual fact, both Friedman and Keynes were using a moribund theory that had no basis in reality (albeit Keynes’ version was far closer to the truth than Friedman’s).

Philip Pilkington: The New Monetarism Part III – Critique of Economic Reason

The report of the Radcliffe Commission was pessimistic in the extreme with regards monetary policy. The commission found that the central bank had little control over the expansion of the money supply and that the velocity of money was extremely variable. Basically, what the commission found was that the banking system was largely passive in relation to the economy. Central banks did not ‘drive’ the economy at all and any policies they did implement, if they were in any way effective at all, would be wholly subordinate to real economic variables such as levels of private investment, consumer demand and government spending and taxation policies.

…

This is arguably where we are today. Quantitative easing is based on the same principles as the monetarist doctrine: increase the money supply and national income will increase with it because the correlations between these two measures can be explained through recourse to a simple, straight-forward channel of causation. And yet once again we have seen the failure of the doctrine – a failure which would have been obvious to Lord Radcliffe and his colleagues. QE has not done what it was supposed to. The banks are flooded with reserves and the money supply has increased drastically, yet national income has not followed suit.

Yet, at the same time, further rounds of QE are still spoken of in solemn tones by central bankers and the media (the markets, however, have been getting a bit sceptical recently…). What’s more, the old monetarist doctrines are still taught in economics departments across the world under the guise of the money multiplier.The entire posts are well-worth reading, as Pilkington describes the significance of the endogenous theory of money while driving a stake through the theory underlying NGDP Targeting (a primary policy goal/tool of New Monetarists today). The logic outlined here is precisely why I continue to be skeptical of QE-based stock rallies and of the many policies put forth by New (Market) Monetarists. Despite numerous refutations of Monetarist ideals and practical failures throughout history, Monetarism lives on. Pilkington concludes:

Now is the time to allow policymakers and the educated public a look inside. Now is the time for a new Radcliffe Commission to investigate the effects of the QE programs. We can be sure that a bipartisan commission of non-economists who seek only the truth – and not confirmation of the biases with which they earn their crust – can tell us what all this monetary shamanism is actually about.

Hopefully the failed theories of Monetarism can eventually be put to rest once and for all.

For those interested in further thoughts on this subject, here is a sampling of my previous related posts: