I’ve been thinking a lot about this over last few weeks when I have the chance to think. It seems like we are on a real estate monetary standard. Much like how we can use assets like gold to create a commodity money system, it seems like we operate our current monetary system as a real estate standard.

Banks create money against real estate assets. We use this money in our day-to-day transactions, without much thought about what stands behind this money, but most loans are for residential and commercial real estate.

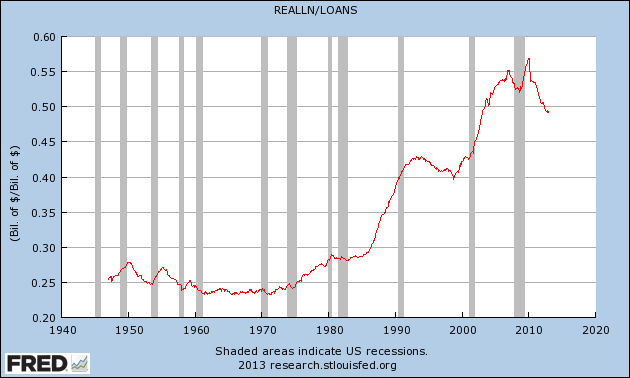

If we did operate under a real estate standard, we would expect to see the larger economic business cycle greatly impacted by the real estate cycle, far more than the declines in real estate activity would predict.The impetus for this discussion is a recent paper by Ed Leamer, “Housing is the Business Cycle,” that confirms Mike’s prediction. The following graph shows real estate loans at all commercial banks as a percentage of total loans and leases:

Notice that the percentage held relatively steady around 25 percent for nearly 40 years following the end of WWII. Then, in the mid-1980’s, the percentage surged higher. This massive change may have been a consequence of the Tax Reform Act of 1986 that included “ increasing the Home Mortgage Interest Deduction,” a “Low-Income Housing Tax Credit,” and changes to “ the treatment of imputed rent, local property taxes, and mortgage interest payments to favor homeownership.” After leveling off in the mid-1990’s, the percentage of real estate loans once again spiked higher beginning in late 1998. Once again, changes in tax policy may have played a substantial role. The Taxpayer Relief Act of 1997 substantially lowered the capital gains rate and “exempted from taxation the profits on the sale of a personal residence of up to $500,000 for married couples filing jointly and $250,000 for singles.”

Notice that the percentage held relatively steady around 25 percent for nearly 40 years following the end of WWII. Then, in the mid-1980’s, the percentage surged higher. This massive change may have been a consequence of the Tax Reform Act of 1986 that included “ increasing the Home Mortgage Interest Deduction,” a “Low-Income Housing Tax Credit,” and changes to “ the treatment of imputed rent, local property taxes, and mortgage interest payments to favor homeownership.” After leveling off in the mid-1990’s, the percentage of real estate loans once again spiked higher beginning in late 1998. Once again, changes in tax policy may have played a substantial role. The Taxpayer Relief Act of 1997 substantially lowered the capital gains rate and “exempted from taxation the profits on the sale of a personal residence of up to $500,000 for married couples filing jointly and $250,000 for singles.” The shifting of bank lending from primarily commercial to real estate loans has clearly been accompanied by shifts in policy to vastly reduce taxes accompanying rents, interest and capital gains. These changes, as well as other public policy initiatives, have helped significantly increase the value of homes that could be borrowed against. As Michael Hudson argues in The Bubble and Beyond, the overall effect has been to transfer former tax payments to private financial institutions, ultimately increasing wealth inequality and making the economy (and government) more beholden to the banks.

Although total real estate loans have actually fallen during the past few years, they still account for nearly 50 percent of total loans. This real estate monetary standard is certainly not restricted to the U.S. and actually appears to be prominent in Europe, as well as several other developed nations. To the degree that bank lending affects aggregate demand, real estate will clearly continue to have an outsized effect on the global business cycle.

(Note: For those interested, Leamer actually discussed this paper during an episode of EconTalk with Russ Roberts back in May 2009.)