My claim is that expected inflation over the next 5 (and 10 and 20) years is very similar to actual inflation over the past year. I think the data generally fit the crudest most mechanical adaptive expectations hypothesis.

This would be interesting for two reasons.

First, the adaptive expectations hypothesis has been treated with utter contempt for roughly 4 decades. It is considered an example of the sort of thing which economists must utterly reject. The effort to replace it has lead to a lot of mildly interesting math and highly implausible assumptions.

Second, there is a huge and very vigorous discussion of forward guidance by the Fed Open Market (FOMC) Committee. It has been argued that even when the Federal Funds rate is essentially zero, the FOMC can stimulate the economy by causing higher expected inflation. It is generally agreed that the FOMC has been convinced by this argument. I think this implies that there should be anonalous increases in expected inflation on the dates when the FOMC began to try to cause higher expected inflation -- roughly the announcements of QE 1-4, operation twist and of forward guidance of how long it will keep the Federal Funds rate extremely low. An excellent fit of expected inflation using only lagged inflation creates serious difficulty for those who think the FOMC always could and finally has promoted higher expected inflation.

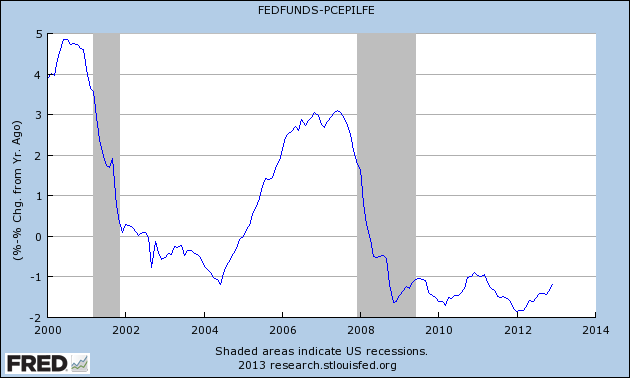

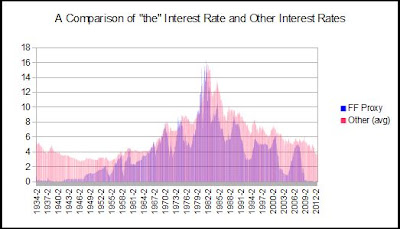

Woj’s Thoughts - This topic is reminiscent of a chain of posts nearly six months ago that began with JW Mason’s inquiry, Does the Fed Control Interest Rates? Jazzbumpa and Art Shipman chimed in with their own opinions, the latter providing this relevant chart on the path of interest rates over time:

Responding to the others’, my view was that:

Responding to the others’, my view was that:

market expectations of future Fed action are sticky. During the post-war period until about 1980, inflation was consistently rising despite mainstream economic views that suggested those conditions would not persist. Following a lengthy inter-war period of near rock-bottom interest rates, market participants were slow to adjust expectations to the actual height of interest rates that would occur before sustained disinflation began. Once disinflation began in the early 1980’s, market expectations were equally slow in recognizing how long disinflation could persist and therefore how low the Fed would ultimately take rates (and hold at zero).Returning to Robert’s claim, I suspect the recent strong correlation between the previous year’s actual inflation and inflation expectations for the next 5 or 20 years is partially due to the lengthy period of low inflation that came prior. In other words, if inflation were to start trending higher or lower over an elongated period, I predict inflation expectations would lag actual inflation while moving in the same direction. The adaptive inflation expectations hypothesis will therefore still hold, only more years of recent data will need to be incorporated into expectations formation. Validation of this hypothesis will deal a serious blow to the perception that Fed communications at the ZLB are an effective form of stimulus.