This data is consistent with rising income and wealth inequality but requires reversing Stiglitz’s “underconsumption” hypothesis. Trying to maintain relative consumption levels, many households clearly chose to rely on previous savings or new debt as a means of temporarily boosting consumption. As inequality continues to rise, wealthy households are now electing to retain more of their savings within corporations. It doesn’t take a leap of faith to suggest this combination of factors depresses aggregate demand.Still unconvinced, Krugman has been searching for further data (see here and here) that would lead him to believe inequality really is holding back the recovery.

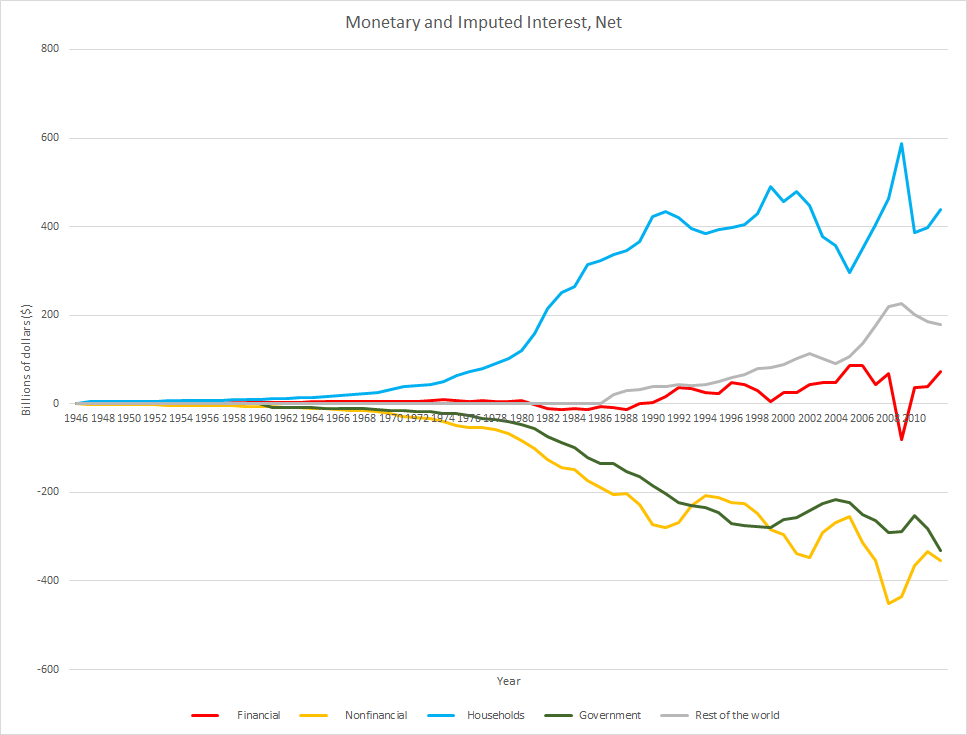

Hoping to aid Krugman in his quest and expand upon my “overconsumption” theory, let me respond to a critique of the previous post. Over at Mike Norman Economics, a commenter (Ryan Harris) kindly noted the obvious omission of interest income and sectoral balances. After sorting through interactive data from the Bureau of Economic Analysis, here are net amounts of monetary and imputed interest by sector [positive (negative) total implies sector receives (pays) net interest]:

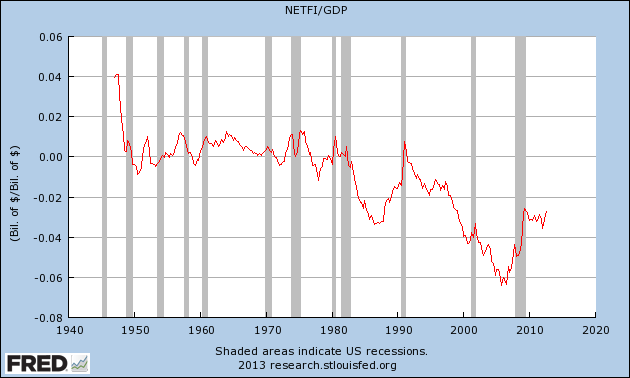

Unsurprising to those familiar with sectoral balance analysis, households net interest position took a sharp turn upwards when federal budget deficits began expanding more rapidly in 1980:

Around the same time, household interest income received a significant boost from the nonfinancial business sector. The pronounced decline in the net interest position of that sector aligns closely with high interest rates of the preceding period and a massive expansion of nonfinancial corporate debt shortly afterwards:

Since then the rise and fall of nonfinancial interest payments (and outstanding debt) has tracked the business cycle, with the overall trend remaining steadily lower (higher net payments and outstanding debt). Although these transfers support household income, they also increase income inequality since wealthy households hold a vast majority of financial assets (including corporate debt).

Turning to the foreign (rest of the world) sector, the U.S. current account (trade) balance fell heavily in the 1990’s:

Foreign countries began amassing large quantities of U.S. financial assets (primarily Treasuries) corresponding to the substantial trade deficits. The growth in net interest receipts arising from these holdings represents an ongoing leak in domestic aggregate demand.

With the beginning of a new millennium and the dot-com bubble, a hostile environment was created for the household net interest position. Federal budget surpluses, declining interest rates, rapidly expanding trade deficits, and increasing payments to the financial sector (for housing) led to a nearly 40% decline in household net interest receipts. Combined with increasing income inequality, many households drew upon savings and increased demand for new debt to maintain previous levels of consumption.

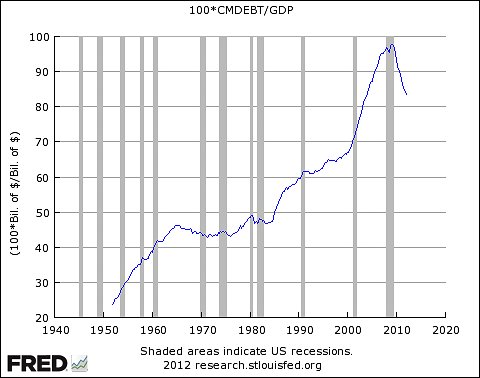

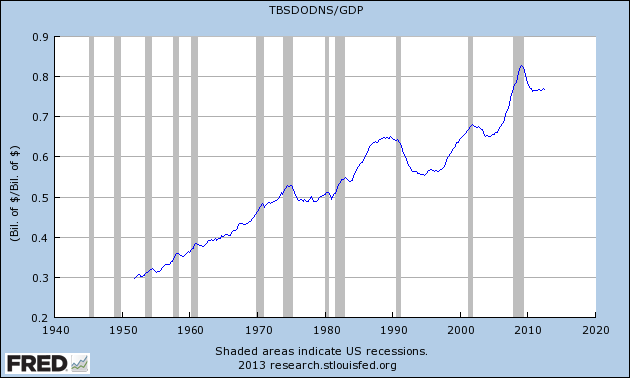

A side effect of the budget surpluses was a growing desire for safe financial assets separate from U.S. Treasuries. Securitization provided a means for new loans of varying risk to be converted into supposedly “super-safe” assets and transferred off of bank’s balance sheets. These factors encouraged banks to meet the surging demand for new loans coming from households (Chart: Household Debt-to-GDP):

The effects of these transactions can also be seen in the transfer of net interest payments from households, and later businesses, to the financial sector. Apart from adding to inequality, these transfers reduce aggregate demand since, as Michael Hudson notes in The Bubble and Beyond, “financial institutions tend to save all their income.” (2012: Kindle Locations 6814-6815)

Since the financial crisis ended, the trend towards higher net interest receipts by the financial sector and greater net interest payments by the nonfinancial corporate sector have returned. These transfers of income up the income/wealth ladder serve to exacerbate the weak demand stemming from two decades of stagnating household interest income. Unfortunately, and so far unsuccessfully, public policy (fiscal and monetary) remains dedicated to originating a new private debt led boom.

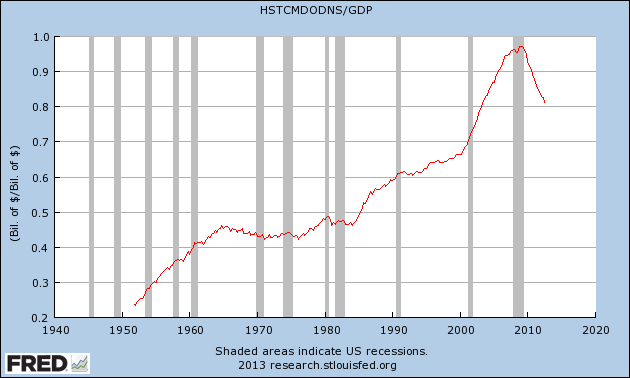

The changes in net interest payments/receipts over the past few decades highlight the growing income and wealth disparities present in our society. For many years households dug themselves deeper in debt to maintain relative consumption levels. The costs of excessively accumulating private debt have now been recognized, but the burden of interest payments suppressing aggregate demand will be felt for years to come.

Bibliography

Hudson, Michael (2012-10-04). THE BUBBLE AND BEYOND (Kindle Locations 6814-6815). ISLET. Kindle Edition.