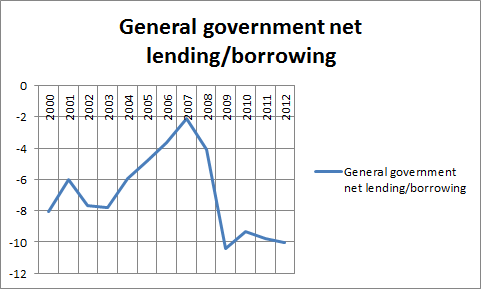

As a DC resident, last week I experienced both an earthquake and a hurricane. Thankfully neither resulted in significant injuries within the impacted areas and property damage was also less than some might have expected. These experiences have provided opportunity for several economists to once again discuss the economic effects of natural disasters. Earlier this year, when Japan was hit by a terrible earthquake and tsunami, numerous economists and market "experts" noted that the destruction would be positive for economic growth due to rebuilding efforts. Similar comments sprung up following Hurricane Irene's treacherous path across the eastern seaboard.

These discussions are precisely when better definitions of economic growth are needed apart from GDP. Based on my understanding, if someone's car was destroyed and they choose to replace the vehicle by purchasing another, that purchase adds to GDP, while the lost vehicle subtracts nothing. From a real world perspective, the person whose car was demolished is now worse off, since they still own only one car but are now out a significant sum of money. Meanwhile, the car salesman is only better off by the amount the other individual spent. On the whole the economy is not better off since the amount of goods remains the same. GDP therefore fails to account for the depreciation or destruction of asset value, which plays a significant role in establishing wealth and economic well-being.

Russ Roberts of Cafe Hayek, who helped create the "Fight of the Century" videos (linked below), provides a wonderful example of what's known as the broken window fallacy. His counterpart on the website, Don Boudreaux, also had a humorous retort to Peter Morici (Professor at University of Maryland) regarding this fallacy and his willingness to destroy property for payment in order to benefit others (

http://cafehayek.com/2011/08/open-letter-to-peter-morici.html). I urge those not familiar with the argument to read the articles and determine which theory is more compelling.

The Microeconomics of the Broken Window Fallacy:

The Keynesian defense of breaking windows or the economic virtues of hurricanes would go something like this:

Yes, breaking windows is destructive. Yes, it reduces wealth. But when there are large amounts of unemployed resources, say in the glass business, then breaking windows is close to a free lunch. In a world of unemployed glaziers, breaking windows can jump-start the economy by putting the unemployed back to work. They will spend the money they receive for repairing the broken windows.

When confronted with the claim by those of us who like Bastiat, that the money to repair the windows will now be unavailable to spend on something else, the Keynesian responds like this:

But people are sitting on money that is doing nothing. The insurance company that will now pay back the homeowner whose house was damaged by the hurricane was sitting on piles of cash. That cash was sitting in the bank where the bank has excess reserves not being lent out, not being invested. So yes, breaking windows can improve the incomes of glaziers and start a process of recovery.

What do we respond, those of us who are enamored with Bastiat and who think he’s right?

I would re-state the Bastiat story and tell it a little differently than it is usually told. The usual point is that the money has to come from somewhere–we see the repaired window but ignore the things that don’t get built or bought. But I think a better way to tell the story is to point out that the RESOURCES have to come from somewhere. The hurricane increases the demand for glaziers and that is good for glaziers. But that is good for all glaziers, employed and unemployed. It pushes up the price of glass repair. That discourages some folks from having glass work done who otherwise would have done it. So there is some offset of the hurricane’s impact on glazier employment. And as the Hayek character says in “

Fight of the Century“:

You see slack in some sectors as a “general glut”

But some sectors are healthy, only some in a rut

So spending’s not free – that’s the heart of the matter

Too much is wasted as cronies get fatter.

So while glaziers (and carpenters) may be unemployed, other sectors (such as the wood market) may not be having such problems. The hurricane has a big impact on the price of wood, discouraging a bunch of would-be demanders of wood from buying as much as they did before. Again, there’s an offset. The point is that “aggregate demand” doesn’t tell the whole story.

But the real problem with breaking windows is that it’s not productive. I know. That’s obvious. But think about what the words mean. Right now, there are a lot of unemployed construction workers. What does a hurricane do? A hurricane IS good for carpenters and glaziers and roofers. But it’s unproductive work. It gets the home owner back to the status quo. It doesn’t create anything new or valuable. I’m not saying the production is wasted. I’m saying it’s a repair. Why is that important?

Imagine a world where there hasn’t been a hurricane and I want to help the unemployed carpenter. Here are two ways to do so. One is to burn my house down and then call the carpenter and give him $100,000 to rebuild my house. Here is the second way. I call the carpenter and say, I feel bad that politicians artificially increased the demand for housing at the end of the 20th century, pulling you into an industry that cannot be sustained at its current leve. I feel bad that you’ve been unemployed for three years. So I’m going to give you $100,000.

Which of those two policies would have the bigger stimulative effect? The charity should have a bigger effect. No offsets from pushing up the price of lumber and so on. But giving people money doesn’t change the underlying problem that there are more carpenters than work available for them. Creating temporary work either by burning down houses deliberatively or accidentally through a hurricane doesn’t change the fact that there are too many carpenters and glaziers relative to demand.

So the hurricane

will put carpenters back to work. But it would be even better if there had been no hurricane and people had just given them a check. Charity is more productive than destroying stuff and paying people to get back to square one.

But the charity approach is what we’ve been doing for the last few years. It’s called unemployment insurance. I know, it’s supposed to be stimulative but there’s no sign that it is. Why would it be? It doesn’t solve the problem that there are too many carpenters.

This is related what Arnold Kling calls “

Patterns of Sustainable Specialization and Trade.” Repairing houses damaged by a hurricane isn’t sustainable. And if I just give carpenters money because I feel sorry for them, that isn’t trade. That’s charity. Both have the same stimulative effect–very little, because they don’t get at the underlying problem. Prosperity is the way we specialize and serve each other, creating products and services that we each value. Destruction cannot be the source of prosperity.