The US economy has had several false starts since 2009, and it’s likely that several tangled factors were responsible for their not lasting longer. It’s reasonable to think that one of these factors was that the initial reflationary effects of these unconventional measures faded, because of doubts about the Fed’s commitment to maintaining accomodative policy during a period of catch-up growth. If such growth threatened to generate above-target inflation, then monetary conditions could be expected to tighten.

The rational-nerdy thing to do was to soften the macho commitment to inflation and commit to a temporary period of inflation-tolerance, thereby balancing the two sides of the mandate — but to do so while retaining credibility on both. But as Harless notes, ceding a little ground on one side could be interpreted as ceding all ground. Being a “macho badass” central banker means credibly committing to never cede ground.

…

All of which has been a long windup to saying that the appeal of the Evans Rule, and if we ever get it, some variation of NGDP level targeting, is this: they institutionalise the macho badassery, which in a dual-mandate framework can only be applied to one of the two mandates.Woj’s Thoughts - This post is reminiscent of a thread from last year involving Steve Roth and Ryan Avent on The Asymmetric Nature of Monetary Policy. In that post I made the following claim:

Whereas Roth suggests that asymmetric credibility stems from the Fed’s actions, I believe it is actually an inherent condition in our current monetary system. The Fed sets the base price for money and credit, but with private banks free to create credit, it holds relatively little control over the total amount outstanding at any time. As growth in the US has exceeded inflation for much of the past three decades, the conditions were ripe for borrowing and credit outstanding now greatly surpasses the sum of base money.

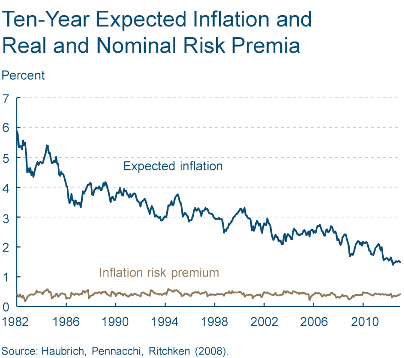

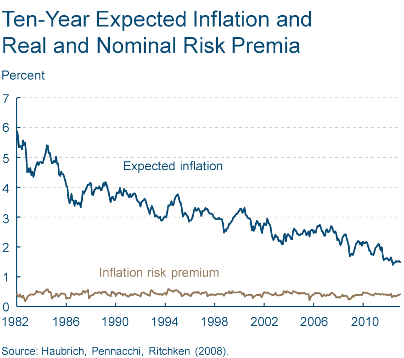

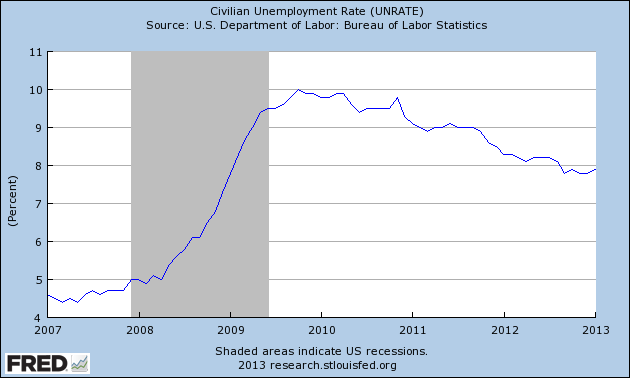

Even if the Fed promised indefinite QE, it’s hard to see the mechanism, aside from adjusting inflation expectations (wealth effects are minimal), by which this would spur real growth. Given the Fed’s skewed abilities and determination to maintain its credibility, it seems more obvious why inflation targeting remains prominent. Further, this may help explain why the Fed downplays its employment mandate (which should be removed anyways). Facing the endgame, the Fed knows it can reduce inflation (and growth) but remains unsure how successful it could be at achieving other targets.Sucumbing to pressure, the Fed has finally decided to cede ground on its commitment to inflation. Unfortunately for the Fed, both inflation expectations and unemployment are not cooperating:

At this point I doubt whether even altering inflation expectations would provide any boost to actual inflation or employment. If fiscal policy continues to contract the budget deficit, these numbers will continue moving in the wrong direction. The Fed has taken a big risk with its established credibility. I fear the results will be very disappointing.