His conclusion is:

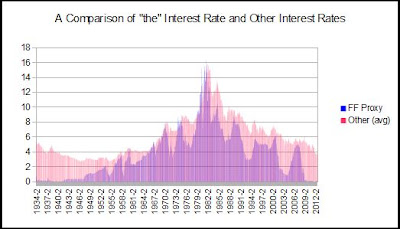

Wouldn't it be simpler to allow that maybe long rates are not, after all, set as "the sum of (a) an average of present and future short-term rates and (b) [relatively stable] term and risk premia," but that they follow their own independent course, set by conventional beliefs that the central bank can only shift slowly, unreliably and against considerable resistance? That's what Keynes thought.So apparently the Fed doesn’t control interest rates. Well, hold on a moment. Not long after Mason’s post, The New Arthurian Economics responded with But why, JW? Why "The past 25 years"?? As you’ll note, the above chart only considers rates back to 1987. Using some clever data mining and chart altering, Art comes up with the following historical look at the Fed Funds rate versus an average of other market interest rates:

Once again, it appears that rates are not following the Fed as closely as one might expect.

Responding to both Mason and Art, in the comments, I offered my own answer to the question. In short (you can read the full comments if you choose), market expectations of future Fed action are sticky. During the post-war period until about 1980, inflation was consistently rising despite mainstream economic views that suggested those conditions would not persist. Following a lengthy inter-war period of near rock-bottom interest rates, market participants were slow to adjust expectations to the actual height of interest rates that would occur before sustained disinflation began. Once disinflation began in the early 1980’s, market expectations were equally slow in recognizing how long disinflation could persist and therefore how low the Fed would ultimately take rates (and hold at zero).

Contrary to this expectations based view, Jazzbumpa, of Angry Bear, countered with a link to his previous post on Who Determines Short Term Interest Rates? His conclusion, supported by various graphs:

The Federal Funds Rate, which is set by the Fed, FOLLOWS 3 month T-Bill rates. It does not lead the economy.This leads to two important questions on the subject:

1) Does the Fed have any real power to influence interest rates?2) What would happen if they attempted to move counter to the market?These questions have plagued me for the past few weeks, but I think I’ve found the answer.

As I pointed out in one my comments:

The Fed acts in certain intervals and operates under a corridor system. In this manner, the Fed sets the target rate but permits fluctuations within a band between the discount rate and IOR rate.Now let’s imagine that during an interval between FOMC meetings, private credit expansion is causing banks to demand more reserves. Absent open market operations that increase the supply of reserves, the Fed Funds rate will move higher towards the upper bound of the targeted range. Witnessing this change, the Fed can choose to respond by either expanding the supply of reserves to maintain its current policy rate or by raising the rate to match the “market-determined” interest rate. The same principle would apply in reverse to a decline in demand for reserves. In this manner, the Fed FOLLOWS the market in supplying reserves and setting the Fed Funds rate.

Not surprisingly, the story above complements the paper by Scott Fullwiler “Interest Rates and Fiscal Sustainability”, which notes:

“More recently, Fullwiler (2003) and Lavoie (2005) have demonstrated that the central bank’s obligation to promote the smooth operation of the payments system means that the provision of reserve balances are necessarily non-discretionary. (p.12)”After much thought, I’m willing to concede that the Fed primarily acts (or has acted) passively in setting short-term rates. This view, however, does not entirely undermine the expectations theory for long-term interest rates or the Fed’s ability to control interest rates. If market participants are aware that the Fed reacts to market moves, then future expectations regarding a “market-determined” interest rate provides a reasonable proxy for the Fed Funds rate. Separately, the Fed could announce a ceiling on long-term Treasury rates and dare the market to test its resolve. Therefore, I accept that in practice the market determines interest rates, but retain the view that operationally the Fed could control interest rates.

A real test of the Fed’s power to manipulate interest rates would require the Fed to either act counter to the market or cap specific rates along the curve. Although the latter seems more likely than the former, I don't expect either action to occur anytime in the near future. Considering central banks outside of the Fed, the ECB may soon provide a real-world experiment by setting a ceiling on rates. Though the EMU holds stark differences with the US monetary system, it will be enlightening to witness a central bank truly take on the markets. This debate is far from over...